5 Takeaways From CALLAHAN & ASSOCIATES Trendwatch 1Q 2024 - Asset quality, liquidity, and revenue are all on the minds of credit union leaders. Here's what the data has to say about that and more.

Credit unions reported record revenue in the first quarter, but delinquency is still up and loan originations are down. Is the industry ready for the year ahead? First quarter data offers a window into what might happen in the year to come.

Takeaway 1: Delinquency Ticked Down

DELINQUENCY BY PRODUCT

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.24

© CALLAHAN & ASSOCIATES | CREDITUNIONS.COM

- Delinquency remained elevated in the first quarter, although it fell slightly from its peak in the fourth quarter. Higher interest rates have made it more difficult for Americans to keep up with loan payments, particularly for credit cards. Americans are putting more purchases on credit and missing payments because of it, and credit unions are bracing for more charge-offs.

- Notably, delinquency is concentrated in just a few categories. Delinquency in new auto and residential real estate, for example, has not jumped like in credit cards.

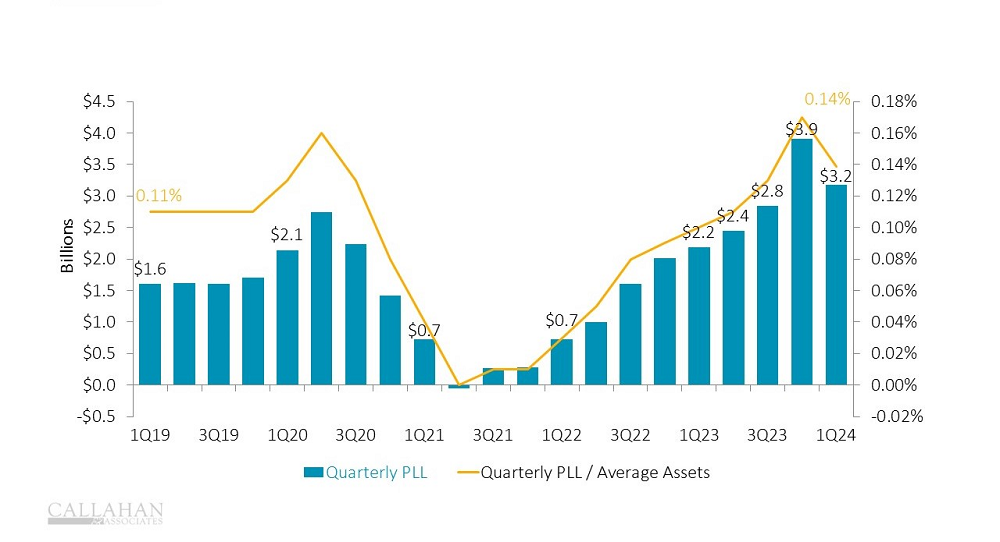

Takeaway 2: Provision Expense Growth Slowed

QUARTERLY PROVISION FOR LOAN & LESS LOSSES

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.24

© CALLAHAN & ASSOCIATES | CREDITUNIONS.COM

- Deteriorating asset quality pushed credit unions to stock up on provisions the past few quarters to guard against future losses. In the first quarter, however, credit unions added $3.2 billion in provisions — a drop from the $3.9 billion added in the fourth quarter of 2023 but still well above the $2.2 billion added in the first quarter of 2023.

- The increase in PLL has dragged down ROA, which dropped from 0.81% in the first quarter of 2023 to 0.66% one year later.

Takeaway 3: Credit Unions Were Less Reliant On Borrowing

BORROWING TO ASSETS

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.24

© CALLAHAN & ASSOCIATES | CREDITUNIONS.COM

- With a loan-to-share ratio of 82.7%, credit unions are feeling the liquidity pinch.

- Borrowing as a percentage of assets increased throughout 2023 as the strategy became a viable alternative to share growth to raise liquidity. However, borrowing is getting more expensive. In the first quarter, the cost of borrowing reached 5.31%, and borrowing dipped slightly.

- Instead, cash from maturing investments became a more alluring option to boost liquidity. In the first quarter, cash as a percentage of assets reached 9.32%.

Takeaway 4: Higher Interest Rates Suppressed Originations

YEAR-TO-DATE LOAN ORIGINATIONS

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.24

© CALLAHAN & ASSOCIATES | CREDITUNIONS.COM

- The pinch of high interest rates forced credit union members to pull back on borrowing in the first quarter. With 30.1% fewer loans made than one year ago, credit unions originated only $113.6 billion — the lowest first quarter origination total in five years.

- This marks the second straight year of sizeable declines; however, the slowdown in real estate mortgage originations ebbed slightly. It fell 9.0% year-over-year, a stark comparison to the 49.5% drop one year ago.

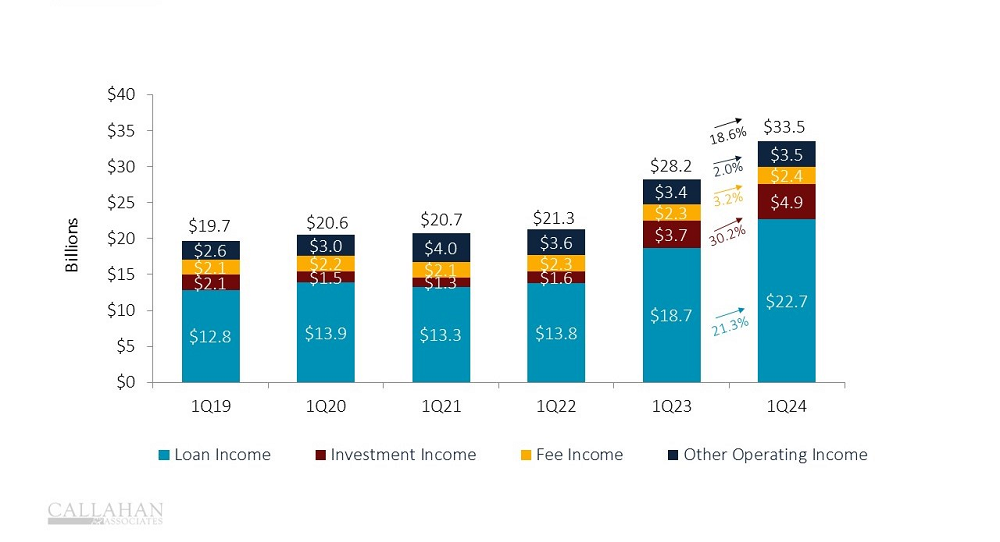

Takeaway 5: Revenue Continued To Climb

TOTAL REVENUE

FOR U.S. CREDIT UNIONS | DATA AS OF 03.31.24

© CALLAHAN & ASSOCIATES | CREDITUNIONS.COM

- Despite the slowdown in loan originations, revenue at credit unions expanded 18.6% year-over-year in the first quarter. Cooperatives capitalized on higher loan yield, and income from loans jumped $22.7 billion. Investment income also climbed 30.2%, a sign that investment securities are repricing at higher rates. All of this means a better starting point for credit union earnings.

- Revenue rose in the first quarter, but so did operating, interest, and provision expenses. Subsequently ROA fell despite the bump in revenue. Keep an eye out for the remainder of 2024 to see how credit unions take advantage of this revenue boost while weathering headwinds.

Comments

Post a Comment

Please no profanity or political comments.