Mortgage Bankers Association and Freddie Mac expect only modest gains this year as the Fed clutches to high interest rates.

Credit/Adobe Stock

Credit/Adobe StockAs the summer heat rises, the prospects for a big 2024 mortgage rally are melting.

Month by month, the Mortgage Bankers Association's forecasts for 2024 originations have diminished to half the gain they predicted a year ago.

In June 2023, the MBA expected total 2024 originations would rise 21% to $2.16 trillion. Its forecast released Monday said it expect this year's originations will rise 9.6% to $1.80 trillion.

Of course, high mortgage rates are the issue, which in turn is a product of the Fed's insistence on keeping rates high until it is really, really sure inflation is reaching its 2% target.

A year ago, the MBA expected 30-year mortgage rates to fall below 6% by December 2024. Now it doesn't expect that will happen until December 2026.

Joel Kan, the MBA's deputy chief economist, said mortgage rates fell slightly to 6.93% last week — their lowest level in three months. The drop in rates helped the number of purchase applications to rise slightly from the week ending June 14 to the week ending June 21 after adjusting for the Juneteenth holiday.

Joel Kan

Joel Kan

"Lower rates, however, were still not enough to entice refinance borrowers back, as most continue to hold mortgages with considerably lower rates," Kan said.

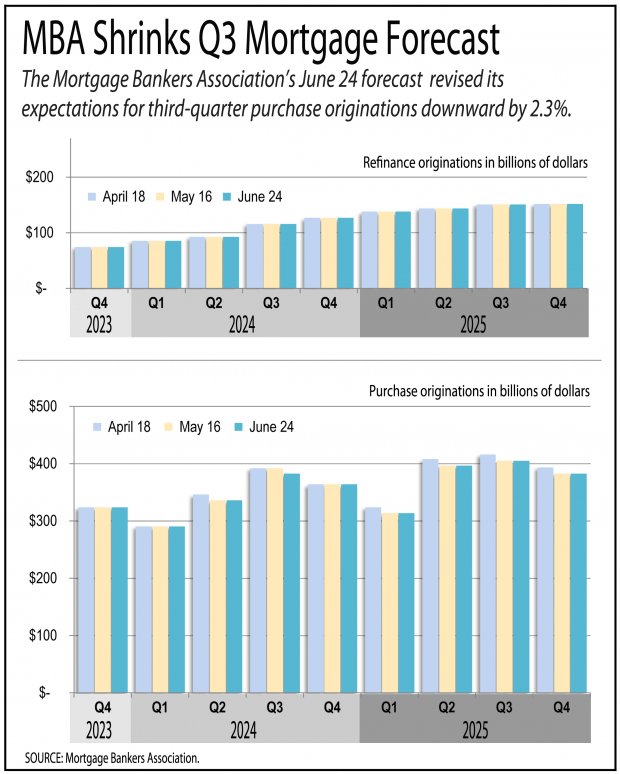

In the June 24 forecast, the MBA made only a small, 2.3% downward revision for third-quarter purchase mortgages. There were no revisions for other periods, and no changes at all in the refinance forecast from the May 18 forecast.

The MBA's June 24 forecast said it expects 2024 originations to rise 3.7% to $1.37 trillion, down from the 12% gain it expected a year ago. Refinances are expected to rise 34% to $422 billion, down from the 51% surge forecast a year ago.

Freddie Mac researchers also said they expect the persistence of high rates to continue to suppress home sales this year. Refinances won't rise out of the basement until rates fall below 6.5%.

"Given persistent inflation, achieving rates below 6.5% is challenging," Freddie Mac researchers said in a June 20 report. "Our forecast suggests a modest increase in total origination volumes this year and next, primarily driven by home prices."

Comments

Post a Comment

Please no profanity or political comments.