But the Mortgage Bankers Association has this year coming up rosier thanks to a big downward revision for 2023.

Credit/Adobe Stock

Credit/Adobe StockThe Mortgage Bankers Association has lowered its forecasts for existing home sales and purchase mortgage originations through the end of 2025 despite interest rates falling and the economy dodging a recession.

But despite steady downward revisions for 2024, this year will look much, much better than last year because of a heavy downward revision for 2023.

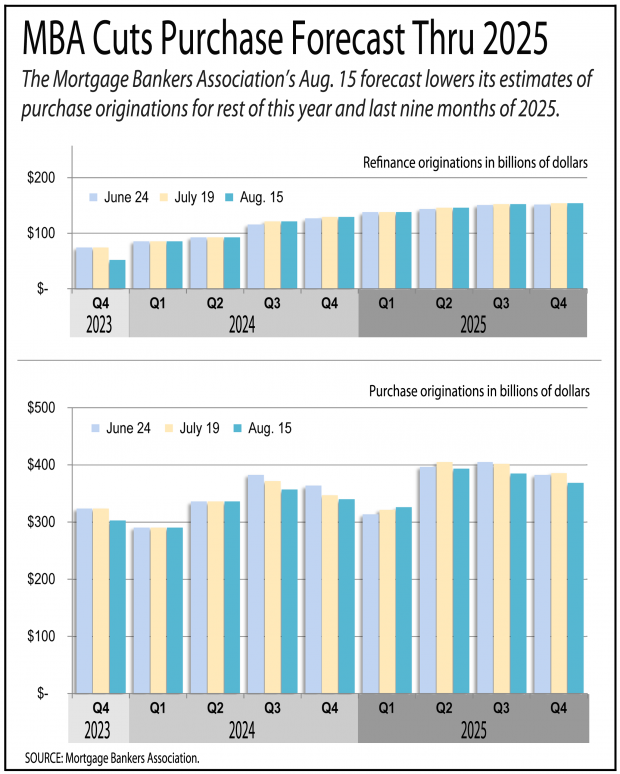

Last year was seen as the pit of mortgage originations with total originations as reported in July at about the level of 2018. With the revision, the pit got deeper with the total now well below 2018 levels. The MBA's July 19 forecast said the total originations were $1.64 trillion in 2023; its Aug. 15 forecast lowers it by 11% to $1.46 trillion.

Purchase originations for 2023 were lowered 6.5% to $1.24 trillion, while refinances were lowered 30% to $219 billion.

And looking out over the next 16 months, prospects are also dimmer for purchases.

The MBA lowered its purchase originations forecasts by 3% for the second half and 3% for 2025. It now expects purchase originations of $697 billion in the second half, up 8.6% from the downward-revised second half of 2023. It expects they will rise 11% to $1.47 trillion for all of 2025.

The MBA made no revisions to refinance originations for this year or beyond. It still expects they will more than double to $252 billion in the second half and rise 37% to $591 billion in 2025.

Falling interest rates goosed the previously moribund refinance market in late July and early August. The MBA reported refinance applications for the week ending Aug. 2 rose 16% from the previous week, and then rose another 35% for the week ending Aug. 9.

The market for purchases remained relatively stuck, rising a seasonally adjusted 1% for the week ending Aug. 2 and 3% for the week ending Aug. 9.

Joel Kan, the MBA's deputy chief economist, said the "refinance index also saw its strongest week" since May 2022 and was 117% higher than a year ago, driven by gains in conventional, FHA and VA applications.

Joel Kan

Joel Kan Kan said the small gain in purchases spanned various loan types, "indicating that prospective homebuyers are slowly reentering the market."

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances fell to 6.54% on Aug. 9, down from 6.82% on July 26.

The MBA is forecasting rates will fall 10 basis points more by the end of the year than it predicted a month ago. It now expects rates will end 2024 at 6.5% and fall to 5.9% by December 2025.

Sam Khater, Freddie Mac's chief economist, said it measured average rates at 6.49% as of Aug. 15, down from 7.09% a year earlier.

"In 2023, the 30-year fixed-rate mortgage nearly hit 8%, slamming the brakes on the housing market," Khater said. "Now, the 30-year fixed-rate hovers around 6.5% and will likely trend down in the coming months as inflation continues to slow. Lower rates are good news for potential buyers and sellers alike."

Comments

Post a Comment

Please no profanity or political comments.