MADISON, Wis. — Credit unions are expected to post stronger loan, deposit, and asset growth in 2026 despite a slowing economy, persistent inflation, geopolitical uncertainty, and continued pressure on consumers, according to TruStage’s latest Credit Union Trends Report.

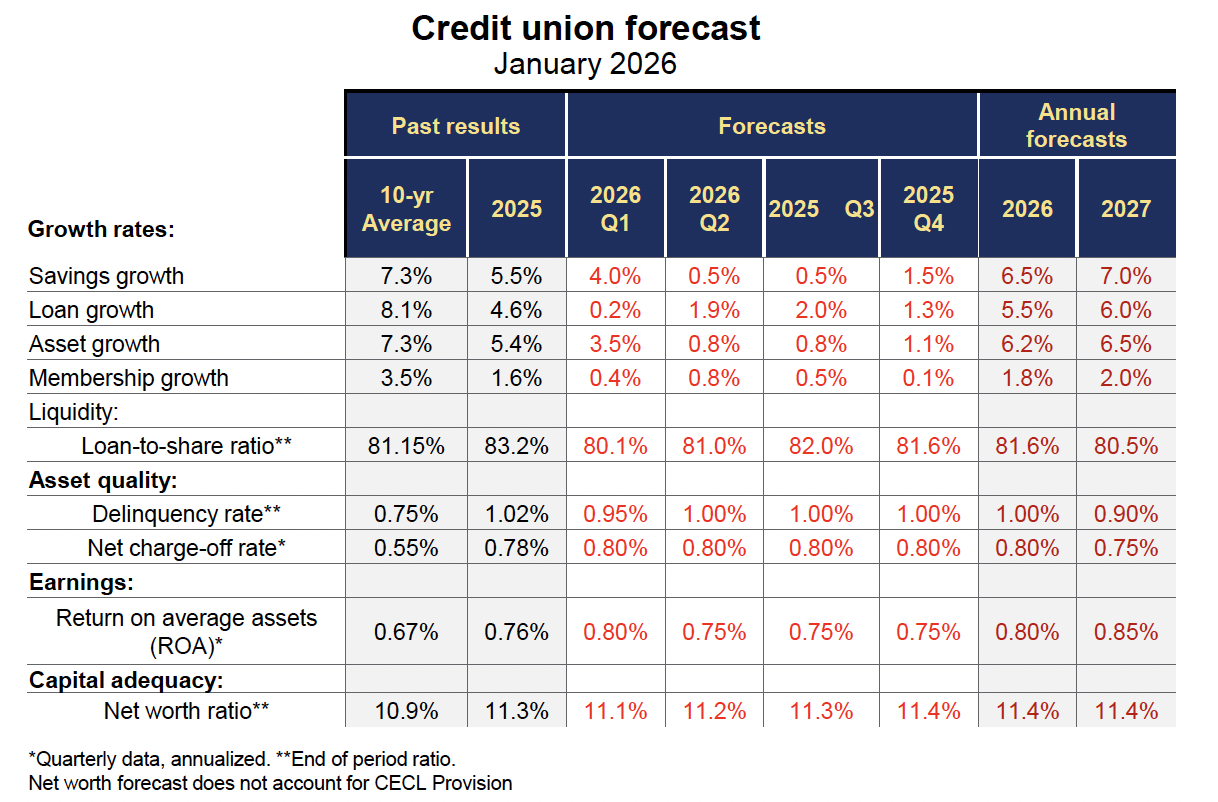

The report, prepared by TruStage Chief Economist Steve Rick and based on December 2025 data, forecasts credit union loan growth will accelerate to 5.5% in 2026 from 4.6% in 2025, while savings growth is projected to increase to 6.5% from 5.5%. Asset growth is expected to improve to 6.2% in 2026 from 5.4% in 2025. Credit union membership growth is forecast to reach 1.8% in 2026 and 2.0% in 2027.

The CU Daily has separate reporting on credit union performance by category here.

According to TruStage, a changing global economic environment has altered its outlook for both the U.S. economy and the credit union system.

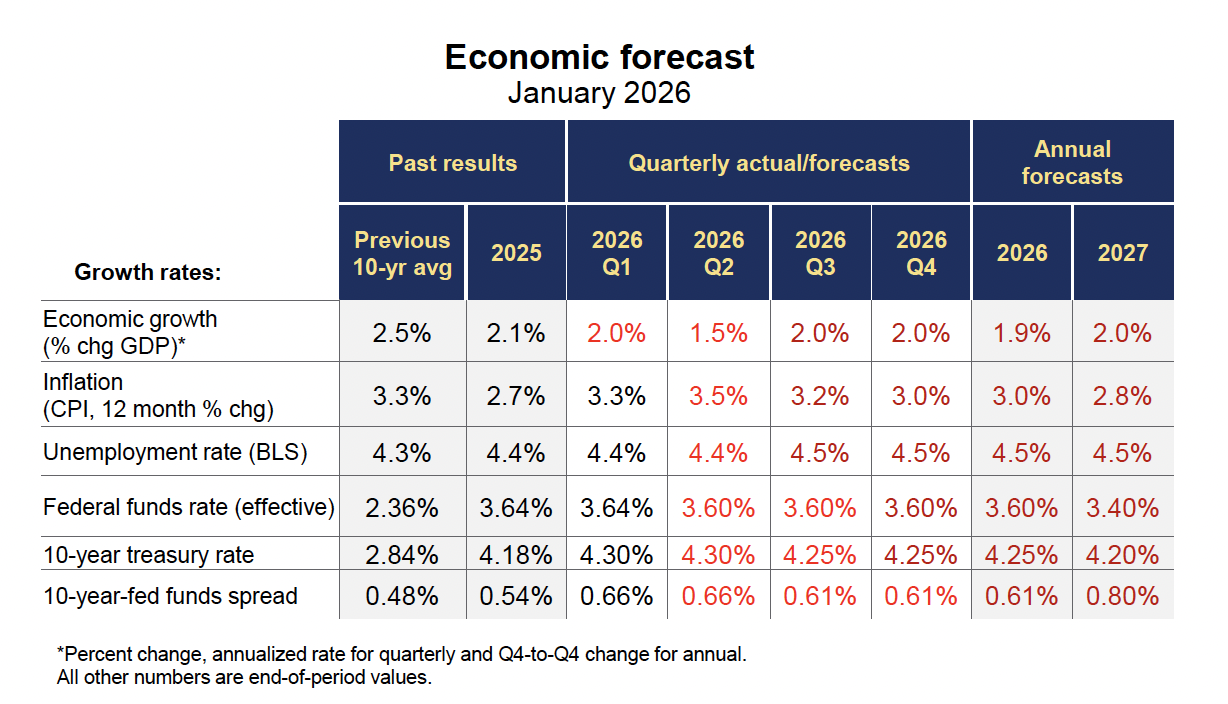

The report noted disruptions stemming from the closing of the Strait of Hormuz have created supply shocks affecting oil, natural gas, fertilizers, helium and industrial chemicals. Those disruptions are expected to increase costs, strain supply chains and reduce economic activity globally. As a result, TruStage lowered its forecast for U.S. economic growth to 1.9% in 2026, down from its prior estimate of 2.4% and below the 2.1% pace recorded in 2025.

Inflation to Remain Elevated

TruStage forecasts inflation, as measured by the Consumer Price Index, will rise to 3.0% in 2026 from 2.7% in 2025 and remain above the Federal Reserve’s 2% target.

The report said higher food and energy prices, tariffs and continued labor-force constraints are expected to keep inflation elevated. As a result, TruStage expects the Federal Reserve to leave the federal funds rate unchanged at approximately 3.6% throughout 2026. The rate is expected to decline modestly to 3.4% in 2027.

The unemployment rate is forecast to remain near 4.5% through 2026 and 2027.

TruStage projects monthly payroll growth will average just 50,000 jobs in 2026, well below the historical average of 170,000 jobs per month, reflecting slower labor-force growth and more cautious hiring by employers.

Long-term interest rates are expected to remain elevated as large federal deficits increase Treasury borrowing needs. The report forecasts the 10-year Treasury yield will average 4.25% in 2026 and 4.20% in 2027. Mortgage rates are expected to remain near 6.4%, keeping the housing market operating roughly 20% below normal levels.

Loan Growth Expected to Improve

Credit union loan balances grew 4.6% during 2025, an improvement from 2.8% growth in 2024 but still below the industry’s long-term average of 7%. According to TruStage, growth was driven primarily by home equity loans, business loans, adjustable-rate mortgages and fixed-rate first mortgages. Consumer installment products such as auto loans, credit cards and personal loans contributed little to overall growth.

The report forecasts loan growth will increase to 5.5% in 2026 and 6.0% in 2027.

TruStage cited four factors supporting improved lending:

- Stronger deposit growth and improved liquidity

- Better loan performance and lower delinquency and charge-off rates.

- Higher capital ratios that provide greater lending capacity.

- Potential reductions in short-term interest rates later in the year.

At year-end 2025, total credit union loans stood at approximately $1.736 trillion. The composition of that portfolio included:

- $630.2 billion in first mortgages.

- $182.3 billion in second mortgages and home equity loans.

- $812.4 billion in total real estate loans.

- $322.9 billion in used auto loans.

- $161.4 billion in new auto loans.

- $484.3 billion in total vehicle loans.

- $88.5 billion in credit card loans.

- $72.9 billion in unsecured loans excluding credit cards.

- $196.2 billion in member business loans.

The data indicate that real estate lending now represents nearly half of all credit union loan balances.

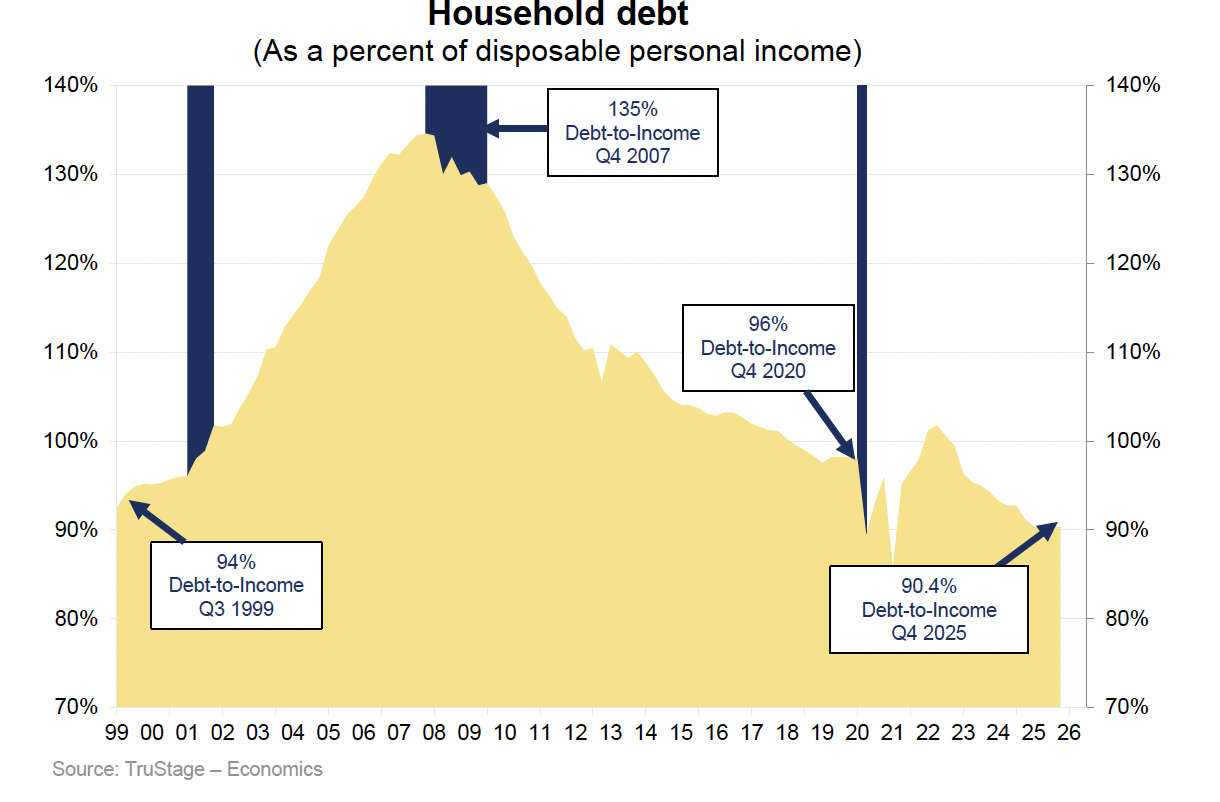

Consumer Debt Burdens Lower Than Past Cycles

The report noted that household debt burdens remain significantly below levels seen before the Great Recession.

Household debt equaled 90.4% of disposable personal income at the end of 2025, down sharply from the 135% peak recorded in 2007 and below the 94% level reported in 1999.

Credit union credit card balances declined at a 1.9% seasonally adjusted annualized rate during part of 2025 as higher borrowing costs discouraged consumers from carrying balances. Consumer installment credit fell 1.0% during the first nine months of 2025, although the decline was less severe than the 1.9% decrease recorded during the same period in 2024, the report states.

For all lenders combined, consumer credit increased only $4.2 billion in November, well below the average monthly increase of approximately $15 billion recorded between 2015 and 2019, according to Federal Reserve data cited in the report.

TruStage expects consumer credit growth to improve during 2026 due to modest job growth, financial market deregulation and lower interest rates.

Comments

Post a Comment

Please no profanity or political comments.