A new YouGov study indicates only one-third of consumers expect to have enough money saved for retirement by age 65, and virtually no one is confident about their plans once they stop working.

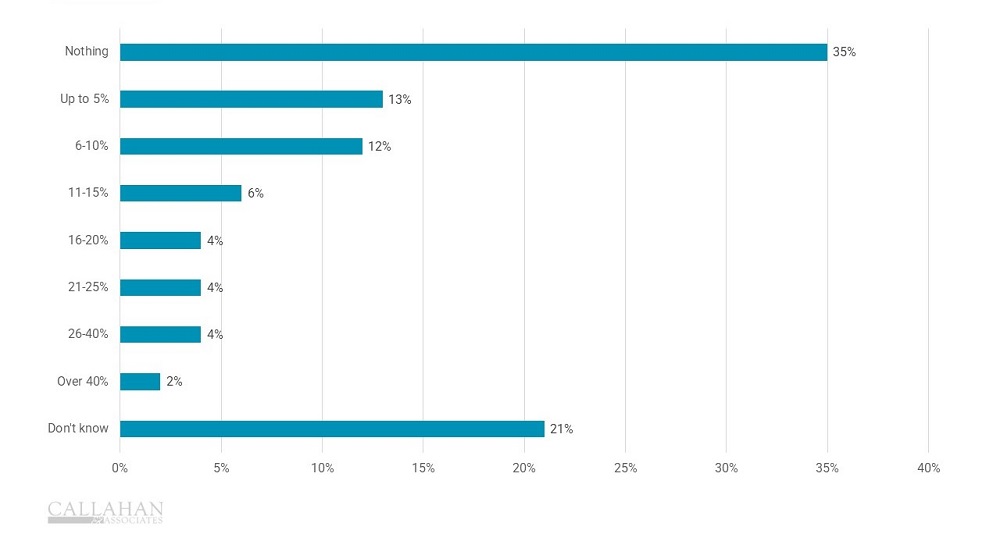

PERCENTAGE OF AMERICANS’ ANNUAL INCOME SAVED FOR RETIREMENT

FOR U.S. CONSUMERS

© Callahan & Associates | CreditUnions.com

Americans want to retire by age 65 — if not sooner. Unfortunately, a majority lack the savings to do so, and a substantial percentage aren’t confident about their financial security once they stop working, according to a 2024 report from YouGov. The average credit union member age has hovered in the mid-40s for decades, and the study’s findings indicate an opportunity for credit unions to lean into retirement-planning services.

Strategic Insights

- Low savings rates: Roughly one-third of Americans believe they’ll be able to retire at age 65, but only 36% believe they’ll have enough independent savings to do so, according to YouGov’s 2024 retirement report. Forty percent of those surveyed reported they aren’t confident about financial security for retirement.

Lack of confidence: The youngest members of the baby boom generation are rapidly approaching retirement age, but 33% aren’t confident they’ll be ready. That figure jumps to approximately 48% for Gen X and millennials.

- Education counts: Regardless of age, those with

post-graduate degrees are most confident about their retirement

finances, but at 49%, even that doesn’t represent a majority.

Respondents with a two-year degree were least confident, though high

school graduates and those with some college experience had similar

responses.

- Taking risks: A majority of those younger than 55

are more likely to take risks with their retirement planning, including

riskier ventures with the stock market and cryptocurrencies.

- An opportunity for credit unions: Roughly 20% of the general population is currently working with a retirement planner or financial advisor.

Comments

Post a Comment

Please no profanity or political comments.