The Widely Cited Mortgage Lending Benchmark 45% DTI May No Longer Reflect How Lenders Evaluate Borrowers, Says Fed Bank

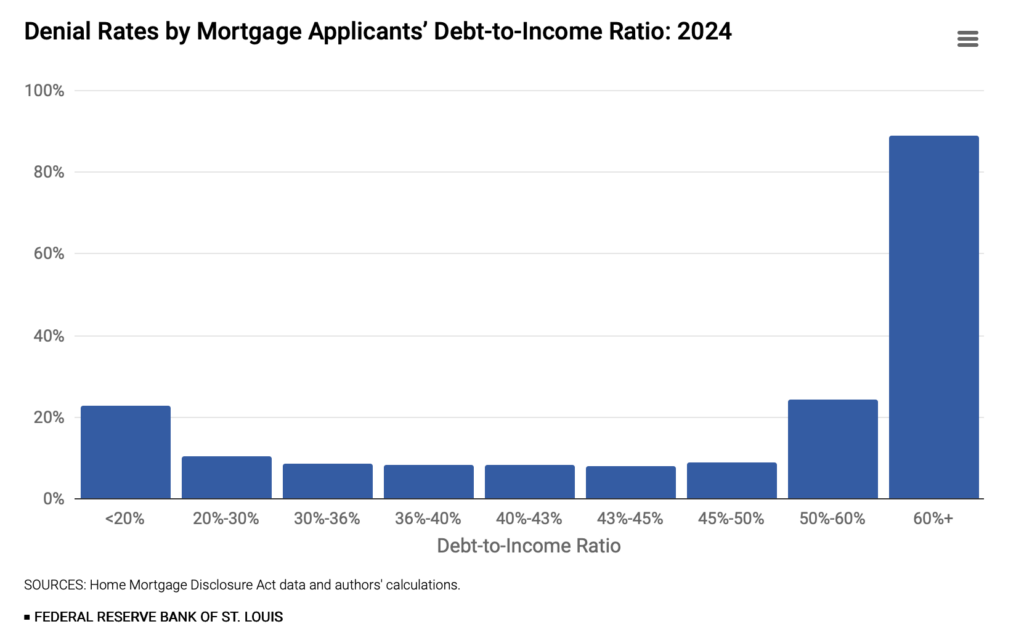

In an analysis of more than 30 million home-purchase mortgage applications filed between 2018 and 2024, researchers found that the long-discussed 43% debt-to-income ratio threshold has little apparent impact on mortgage approval decisions. Instead, denial rates begin to rise sharply once applicants exceed a debt-to-income ratio of 50%.

The findings were published as part of a four-part series examining barriers facing prospective homebuyers.

‘Practical Lesson is Clear’

“For borrowers, the practical lesson is clear: A debt-to-income ratio of 45% is treated by lenders much like a ratio of 35%,” the researchers wrote. “But crossing 50% changes the game entirely.”

The 43% debt-to-income ratio gained prominence under the 2010 Dodd-Frank Act, which established it as a key threshold for so-called qualified mortgages. Loans meeting that standard provided lenders with legal protections against ability-to-repay lawsuits. However, in 2021, the Consumer Financial Protection Bureau replaced the ratio-based standard with a pricing-based approach amid concerns that the 43% cap was unnecessarily restricting access to credit.

Despite the regulatory change, mortgage lenders and personal finance experts frequently continue to cite 43% as a guideline for borrowers.

‘Little Evidence’

The St. Louis Fed analysis found little evidence that lenders treat 43% as a meaningful cutoff.

Using Home Mortgage Disclosure Act data, researchers found mortgage denial rates remained relatively stable between debt-to-income ratios of 20% and 50%, generally ranging between 8% and 10% in 2024. No significant increase in denials was observed at the 43% mark.

By contrast, denial rates rose sharply once debt-to-income ratios exceeded 50%, eventually surpassing 80% for applicants whose ratios exceeded 60%, according to the research.

Additional Tests Conducted

The researchers also conducted statistical tests to determine whether borrowers or lenders were clustering applications below the 43% threshold. They found no evidence of such behavior.

In addition, regression discontinuity analysis showed that denial rates increased by less than one-half percentage point at the 43% threshold. At 50%, however, denial rates jumped by between 15 and 17 percentage points.

“The 43% mark that has drawn enormous regulatory attention barely registers in actual lending decisions,” the researchers wrote. “The 50% mark, which has received no comparable scrutiny, is where applications hit a wall.”

=================================================

Remember, you're not alone with NCOFCU.org

|

Comments

Post a Comment

Please no profanity or political comments.